When the Bills Don't Stop Coming: A Real Family's Guide to Surviving the Financial Side of a Child's Hospitalization

The moment a parent hears that their child needs to be hospitalized, money is probably the last thing on their mind. And yet, within days — sometimes hours — the financial reality of a prolonged hospital stay starts to press in from every direction. There are co-pays, parking fees, meals grabbed on the run, and a job you may not be able to show up to. Then come the Explanation of Benefits documents, the bills that look like invoices but say "not a bill" at the top, and the actual bills that are very much bills.

At Ronald McDonald House Charities of NC, we see this every single day. Families arrive at our Houses exhausted and scared, and many of them are also quietly terrified about what this is going to cost them. The good news? There are real, concrete steps you can take — even in the middle of a crisis — to protect your family's financial health while you focus on your child's physical health.

This guide won't sugarcoat the challenges, but it will give you a roadmap.

Step One: Don't Wait — Call Your Insurance Company Today

One of the biggest mistakes families make is assuming their insurance company will handle everything automatically. They won't — at least not always. As soon as you know your child will be admitted for an extended stay, call the member services number on the back of your insurance card and ask specifically about:

- Pre-authorization requirements for procedures, imaging, or specialist consultations

- In-network vs. out-of-network providers, especially if you've been transferred to a children's hospital that may have different network agreements

- Case management services — most major insurers offer a dedicated case manager for complex or long-term hospitalizations who can help coordinate benefits and flag coverage issues before they become denied claims

- Your out-of-pocket maximum, which is the most you'll have to pay in a given year before insurance covers 100%

Take notes during every call. Write down the date, the representative's name, and a summary of what they told you. This documentation can be invaluable if a claim is later disputed.

Step Two: Talk to the Hospital's Financial Counselor Immediately

Every major children's hospital in North Carolina — including UNC Children's, Duke Children's, Atrium Health Levine Children's, and Brenner Children's — has a team of financial counselors or social workers whose entire job is to help families navigate costs. These folks know about programs that never make it to Google search results.

Ask about:

- Charity care programs: Most nonprofit hospitals are required to offer financial assistance to qualifying families. Income thresholds are often more generous than people expect.

- Payment plans: Hospitals can typically arrange interest-free or low-interest installment plans, but you usually have to ask.

- Medicaid enrollment: If your child doesn't already have Medicaid coverage, a hospitalization may qualify them. Hospital financial counselors can often help you apply on the spot.

- Supplemental programs: Many hospitals have their own emergency funds or connections to local nonprofits that can help with non-medical costs like housing and transportation.

"Parents are often so overwhelmed that they don't realize they have options," says one financial counselor who works with pediatric families in the Charlotte area. "My first goal is always just to get them to slow down enough to hear what's available."

Step Three: Build a Crisis Budget — Even a Rough One

Budgeting during a hospitalization feels counterintuitive. Everything is unpredictable. But even a rough sketch of your monthly income versus your new expenses can help you make smarter decisions and identify where you need the most help.

Start by listing your fixed monthly obligations: rent or mortgage, utilities, car payment, insurance premiums. Then estimate your new hospitalization-related costs: gas or transit to and from the hospital, meals, parking (this alone can run $15–$25 a day at major medical centers), and any childcare for siblings at home.

Next, look honestly at your income. If one parent has had to stop working or reduce hours, calculate that impact. If your employer offers Family and Medical Leave Act (FMLA) protections, make sure you've filed the paperwork — FMLA won't pay you, but it protects your job while you're away.

Some families find that staying at a Ronald McDonald House dramatically changes this budget picture. Our Houses charge no more than a small nightly donation — and for many families, nothing at all — which can save hundreds of dollars a week compared to hotel stays near the hospital.

Step Four: Explore Every Assistance Program Available to You

Beyond hospital-based resources, a network of local and national programs exists specifically to help families in medical crisis. Here's a starting point:

- Patient Advocate Foundation: Offers case management and financial aid for families dealing with chronic or serious illness. Visit patientadvocate.org.

- HealthWell Foundation: Provides grants for families who can't afford their share of treatment costs.

- NeedyMeds.org: A searchable database of patient assistance programs, including medication cost programs.

- 211 NC: Dialing 2-1-1 in North Carolina connects you with a local specialist who can identify food assistance, utility help, rent assistance, and more.

- Your employer's EAP: Many Employee Assistance Programs offer emergency financial counseling or short-term loans that employees never think to use.

- Community organizations: Churches, civic groups like the Rotary Club or Kiwanis, and local foundations often have emergency funds. It's worth a call.

Don't let pride get in the way. Every family we've ever worked with at RMHC of NC wished they'd asked for help sooner.

Step Five: Protect Your Credit During the Storm

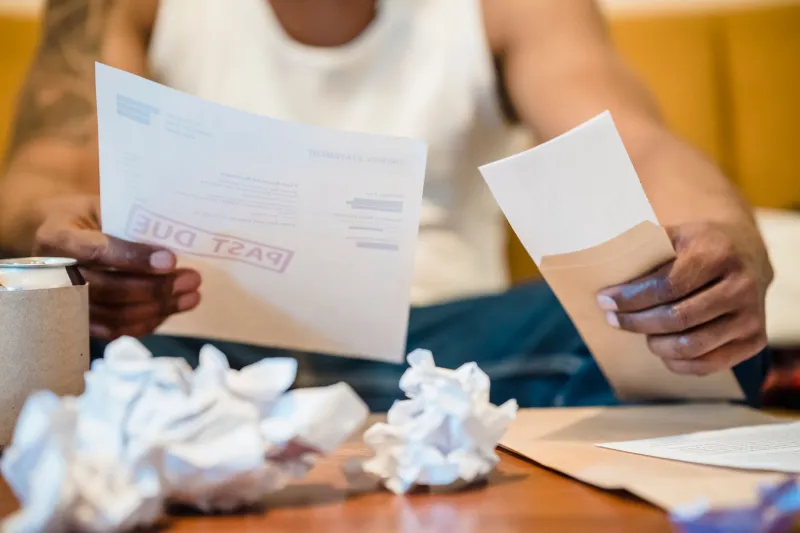

Medical debt is the leading cause of personal bankruptcy in the United States. But there are specific protections and strategies that can keep a hospital stay from derailing your credit for years to come.

- Don't ignore bills — even if you can't pay them. Call the billing department and explain your situation. A $25/month payment arrangement is almost always better than a collections account.

- Know your rights under the No Surprises Act: As of 2022, federal law limits surprise billing from out-of-network providers in many situations. If you receive an unexpected bill from a provider you didn't choose, you may be able to dispute it.

- Request an itemized bill and review it carefully. Medical billing errors are common — studies suggest they occur in the majority of hospital bills. Charges for services not received, duplicate entries, and upcoding are all worth flagging.

- Medical debt and credit scores: As of 2023, paid medical debt no longer appears on credit reports, and unpaid medical debt under $500 has been removed from reports by the three major bureaus. This is meaningful protection for families in crisis.

Step Six: Think About Recovery — Not Just Survival

Once the acute crisis has passed and your child is on the road to recovery, the financial rebuilding process begins. This is the right time to:

- Schedule a session with a nonprofit credit counselor through the National Foundation for Credit Counseling (NFCC). They offer free or low-cost services.

- Revisit your emergency fund goals. Most financial advisors recommend three to six months of expenses saved. A hospitalization makes painfully clear why.

- Review your insurance coverage during the next open enrollment period. Consider whether a Health Savings Account (HSA) or a supplemental insurance policy (like hospital indemnity insurance) makes sense for your family.

Recovery takes time — financially and emotionally. Be patient with yourself and your family.

You Don't Have to Figure This Out Alone

At Ronald McDonald House Charities of NC, our mission has always been to keep families close during the hardest moments of their lives. That means more than just a bed near the hospital. It means connecting families with resources, reducing daily costs, and making sure parents can focus on what matters most: being there for their child.

If your family is currently navigating a child's hospitalization anywhere in North Carolina, reach out to us at rmhcofnc.org. We're here — and so is a whole community of people who understand exactly what you're going through.